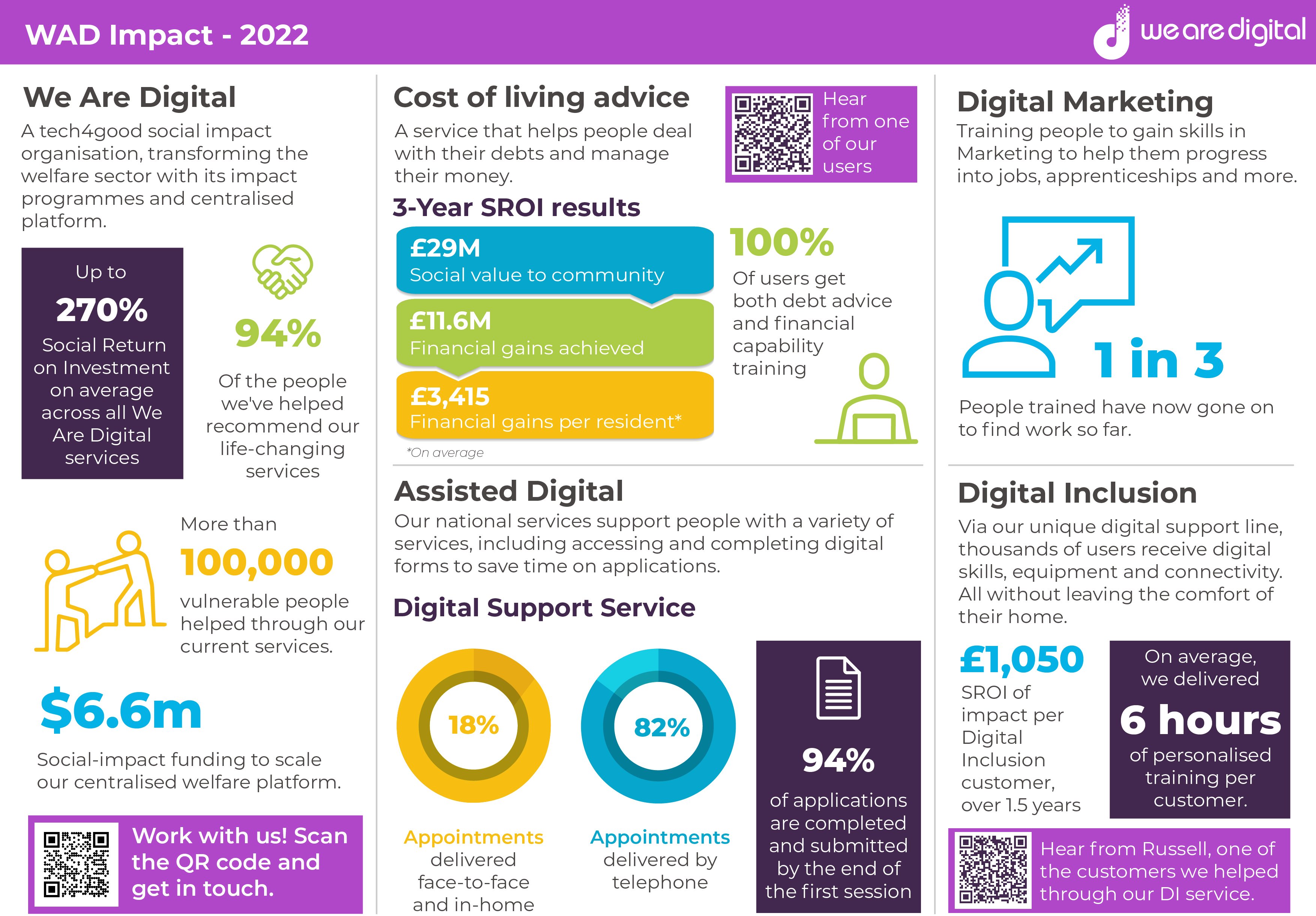

Watch Chris's talk about the Consumer Duty Act for Digital Leaders Week above and read more about the new legislation below.

Many people reading this will be aware that the Consumer Duties Act (CDA) will start to come into fruition in June 23, this piece of Financial Conduct Authority (FCA) legislation has been in consultation for some time although for the general consumer this will not be common knowledge.

Interestingly this legislation is about bringing the customers rights and the obligation of financial sector organisations to the consumer to the forefront of an organisation's agenda.

As a passionate advocate of inclusion, whilst reading and analysing the consumer duties act a couple of things stood out to me, especially regarding the digitally excluded, section 9 which refers to customers and mentions allowing people to have their “channel of choice”.

So, my first question is …1) What is the channel of choice? When are consumers forced to use the channel of necessity?

Take an organisation that has an online service with customers that for some reason are excluded (be that device, data, or skills exclusion) as there are 10.2 million people in the UK according to the Lloyds Bank Consumer Digital Index without foundation skills alone. Well, they can use the phone number you may say, but are they using the phone number because they want to or because they must?

What if the customer would like to be able to use the online service? All of us that can use apps and web-based services understand the ease, speed, and the ability to be able to interact with them at a convenient time.

A lot of us could think of nothing worse than being on hold and listening to the pan pipe music with the repeating “ your call is important to us” message! So what if those that are digitally excluded had a channel of choice that was in fact the digital channel but they are forced to use a channel of necessity….. the contact centres!

A lot of us could think of nothing worse than being on hold and listening to the pan pipe music with the repeating “ your call is important to us” message! So what if those that are digitally excluded had a channel of choice that was in fact the digital channel but they are forced to use a channel of necessity….. the contact centres!

Add to this the “treating customers with fairness” statement in the act. And so, my second question is this 2) is it fair that a service is offered by an organisation that cannot be used by all?

How would you feel if you went into a high street store and were told you cannot use the automated tills because you do not know how to use them, but other people can because they know how, forcing you to stand in a long line and wait to be served. Is that fair? Think about supermarkets, do they have an attendant that will help you use the automated tools…. YES (and to stop under aged people buying something they should not, granted) but why have places like supermarkets offered channel of choice and education on how to use the channel of choice and other large corporation have not. If the fairness and channel of choice aspects of the act holds true, then is not it the responsibility of an organisation who offer any service to make it available to ALL and facilitate those who wish to use it to use it?

Another interesting part that stands out is something called sludge practice, where it is easier to buy a product or join a service than it is to engage subsequently about it afterwards. We all hate being in call centre ques and if you work irregular hours or only have limited window to contact a call centre can you always guarantee we will be able to interact with the supplier…. Definitely not! So, it is in the customers and the organisations interest to facilitate them to engage digitally to allow for channel or choice and to reduce sludge practice.

With sections 9 & 10 PS22/9: A new Consumer Duty being concerned with customer vulnerability, fairness, and openness I was surprised to see mention of identification of the vulnerable but next to nothing about how these highlighted vulnerabilities are actioned. Is it enough to simple maintain a register? Does that truly help the consumer? If an organisation knows that a customer has a vulnerability is there not a responsibility to do something about it? From a human standpoint I would argue yes, and when an organisation is profiting from having that vulnerable person as a customer I would personally state …. definitely! There are complications I am aware of with respect to data and permissions and this is where a digital helpline can really help as it triages the needs and complexities of the customer based on their unique lives .

Those of you from an organisation that falls under the Consumer duties act might think, what business implications are there to enabling people to use an online service that are digitally excluded? And yes, initially from a business perspective I get the thought process “how much is it going to cost” but this is where profit meets purpose. A business can do well and do good at the same time. In short, we know that improving customer experience for people via digital helps them and supports the organisation to save costs and support the most vulnerable at the same time.

Digital Support Helplines also reduces the contact centre volume, decreases the average handling time, and removes sludge practice with more availability for the people whose channel of choice is still the telephone. For the customer, it would increase satisfaction, retention and give the channel of choice. Win/Win in my books! This would be of benefit to other sectors too, Utilities for example.

So, what qualifies me to have an opinion on this I hear you ask?

Because at We Are Digital, we do this daily for our customers and partners in the financial sector like Lloyds Banking group as well other public and private sector organisations such as L&Q We offer services that are specifically designed to include not only the digitally excluded but also the financially vulnerable by delivering digital and financial support helplines as well as assisted digital services.

We enable an integrated triage service directly taking consumers at the point of interest/crisis warmly from contact centres or through a dedicated contact number so the correct inclusion and customer treatment journey can take place. To expect a customer to only have one option of travelling to a destination for a set time on a set day at personal expense to receive weeks of “training” just to use your services does not seem “fair” so our unique methodology enables customers to choose what is right for them, that could be a branch or a community centre or from the comfort of their own home.

We can also report on service impact which can fed into the regulators as evidence for the Consumer Duties Act compliance, our data can show the FCA how many customers Identified as digitally or financially vulnerable have been helped, when, where and how including the outcome and over time. Add to that the Return on Social Investment (SROI) calculation that is calculated from the data and gives a personal and local community impact, there is a clear indication of the societal impact this service provides which is helpful for CSR teams as well as customer service metrics in the commercial and customer transformation departments.

This all means organisations can enable people to use their channel of choice, operate a digital service with fairness and accessibility for all, reduce sludge practices, reduce call volumes, reduce average handling times, and support the vulnerable all while compiling with the consumer duties act effectively and efficiently. The Consumer Duty Act is a strategic opportunity to do well and do good and I would really love to chat and hear your thoughts. Please feel free to reach out and email me at christopher.gale@we-are-digital.co.uk